Samsung has launched its Samsung Pay product into Australia today, making our country the fifth market where the mobile payment product has been launched. The journey doesn’t stop there, with Singapore launching tomorrow, and additional markets (including the UK, Canada and Brazil) coming by the end of the year.

But what is it?

Samsung Pay enters a somewhat crowded mobile payment marketplace in Australia; the banks have launched their own mobile payment apps in the last year or so, including those from Commonwealth Bank and National Australia Bank, and those from technology vendors such as Apple Pay and the anticipated (but not yet launched) Android Pay service.

It works (just about) everywhere

There are a few points of differentiation, though. For starters, Samsung Pay doesn’t rely solely on NFC for payments, unlike most competing products. In Australia, most payment terminals do accept tap and pay payments, but elsewhere that isn’t always the case. Having travelled quite a bit in the US, tap and pay is far from ubiquitous, and the ability to pay some other way on mobile is welcome.

Samsung Pay’s answer is MST, or Magnetic Secure Transmission. This allows Samsung Pay to transmit — securely, we might add — your payment details to just about any electronic payments terminal, either via NFC or through communication with the magnetic swipe reader.

This contrasts with the banks’ own Tap and Pay apps, which all rely on NFC technology; where contactless payments aren’t supported, those mobile payment apps simply won’t work, and this is Samsung Pay’s major point of difference.

Samsung Pay is built on three pillars, of simplicity, security and the ability to work anywhere. MST and NFC paired will almost address the ‘work anywhere’ aspect by themselves, but simplicity and security have always been a bit hit and miss in mobile payments.

Simplicity

Most of us who’ve used mobile payments in Australia can attest to it being far from a reliable experience; I use NAB Tap and Pay quite frequently, and probably 30-40% of the time, the first attempt doesn’t work, either due to a bad NFC read, or the differing locations of NFC readers in payment terminals. The worst experience is where NFC fails, and the terminal then asks you to swipe or insert your card; something which undoes mobile payments’ benefits completely. Samsung Pay should address this, allowing users to pay with MST if NFC doesn’t work for some reason.

Security

Security is also key, with Samsung Pay being built on top of Samsung’s widely certified Knox platform. There are other security aspects built in, which Samsung can achieve by controlling both the software and hardware. For example, a security fuse in Samsung devices which is tripped when the phone is jailbroken or rooted, preventing access to Samsung Pay data. In short, if your phone is pinched, your data is secure (and can be remotely wiped quite easily).

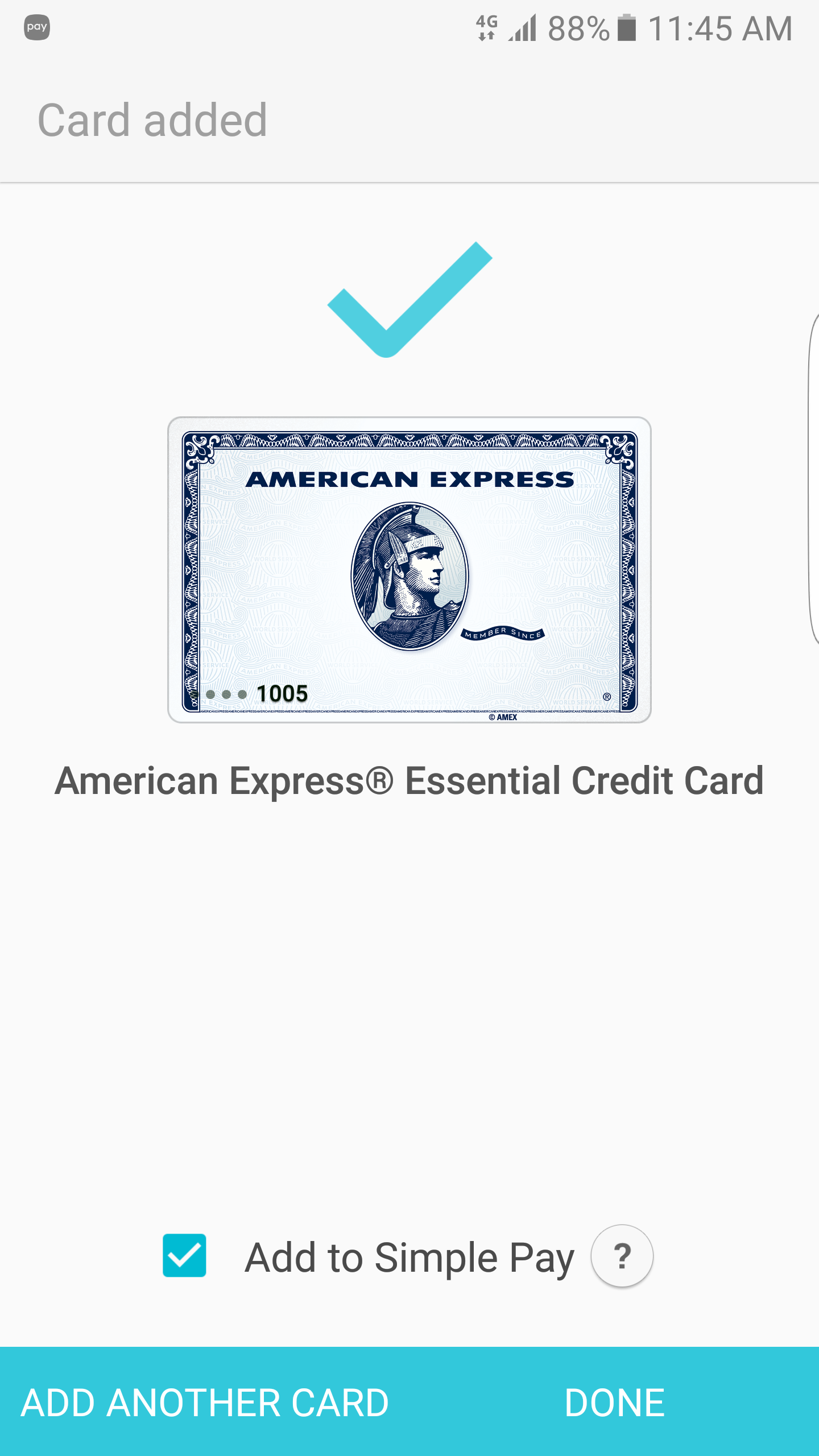

Launch Partners – Citibank and American Express

At this point, Samsung Pay’s launch partners in Australia are Citibank and American Express, and Samsung’s Elle Kim, Vice President of Samsung Pay, tells us that she is keen to see other banks and networks get on board. This is something Samsung appears to be working towards, with an open, accessible partnership model which saw full adoption in Korea, and they hope will see the same take-up here.

American Express have an incentive in place for their card members, so people can try out the Samsung Pay experience for themselves. If cardmembers pay three times using Samsung Pay, of at least $5 per payment, they will receive a $15 credit on their statement after the three payments are made, allowing a fairly risk-free way of trying it out. This will be available until 14 September 2016.

Citibank customers will be able to use their cards with Samsung Pay too; at this stage, we’ve seen demos using Citibank MasterCard, but there’s no mention of restriction just to MasterCard in the launch information — Visa may well be available too. As a means of incentive, Citibank’s existing credit card customers earn 5% cash back on the first $500 spent with Samsung Pay between 15 June and 9 August 2016. There’ll be more info on this on Citibank’s website.

Samsung has been working with Australian partners for around three years in this space, and they seem enthusiastic about the possibility of getting more main-stream card issuers and banks on board soon (but there’s nothing concrete to announce today).

Samsung has a good value proposition for the banks with Samsung Pay, in that — unlike Apple — it doesn’t charge them anything to participate. Samsung’s business model is to drive sales of its phones, as opposed to making money purely from being a financial services intermediary. With this, hopefully, we’ll see the banks jump on board.

What else will Samsung Pay offer?

While payments on wearables are available in other markets, that won’t be on offer here, at least not at the moment. In Korea, Samsung Pay users can pay using their compatible wearables (presumably including the Gear S2 range) and there is the hope that this will become available here.

Outside of payments, Samsung Pay has the potential to be integrated with an array of partners, ranging from major retailers to government departments and ticketing companies. In the US, partners include major retail brands, pharmacies, and more.

Partner integration is even simpler with Samsung Pay because the technology utilises Near Field Communication (NFC) and Samsung’s proprietary technology called Magnetic Secure Transmission (MST), making it the only payment solution with wider acceptance. This use of MST could see partners on board where magnetic stripe is the method they use, including loyalty cards, gift cards and even transit cards.

Transit integration would be a great killer feature in Australia, with Opal and Myki being two rather popular contactless travel payment methods. Of course, there’s a bit more to just simple NFC to make Myki and Opal work, including a range of different security issues; there’s a lot of work going on behind the scenes to explore whether transit integration will be possible in Australia.

I use the tap-n-pay from Heritage and Commbank regularly. Some places it doesn’t work at all, rarely do I need to tap twice. Usually its the older style EFTPOS machines….like my local IGA have, that play up for me. (using a Note 4 btw)

So if you read the fine print MST that was such a big selling point for the prior generation “S6 and S6 Edge” are now being skipped over and just offered as NFC? I have kind of got used to this kind of bait and switch with technology companies but seriously, what is up?

I don’t really know whether a NAB American Express card is meant to work with Samsung Pay or not but I can confirm it doesn’t. Back to NAB tap and pay then…

What a real shame that only AMEX and Citibank are currently supported! Hopefully the other banks jump on board and support Samsung Pay shortly in the future. In the meantime, I use ANZ Mobile Pay on my S7 Edge and it seems to work well with most NFC supported payment terminals.